Broadcom's AI semiconductor revenue hit $10.8 billion in the second quarter, up 143% year-over-year. The stock fell 15% anyway. CEO Hock Tan projected $16 billion in AI chip sales for the third quarter—strong by any historical measure, but $1.2 billion below what Wall Street had penciled in, according to Bloomberg. That gap, roughly the GDP of Belize, wiped out $270 billion in market capitalization across the semiconductor complex on Thursday and sent Micron down 7% despite no company-specific news.

The miss matters because it signals something more fundamental than a single earnings disappointment. Broadcom's AI semiconductor revenue forecast of $16 billion for the fiscal third quarter fell below analysts' expectations of $17.2 billion, and CEO Hock Tan said the company will sell $56 billion worth of AI chips in the fiscal year ending in October, also falling short of estimates . The bar had been set so high that even triple-digit growth couldn't clear it. Broadcom had added roughly $270 billion in market value over the previous five trading sessions , driven by optimism that the company could challenge Nvidia's dominance in custom AI accelerators. When the guidance came in light, the entire AI hardware thesis got repriced in real time.

Can Memory Makers Keep Up With Demand?

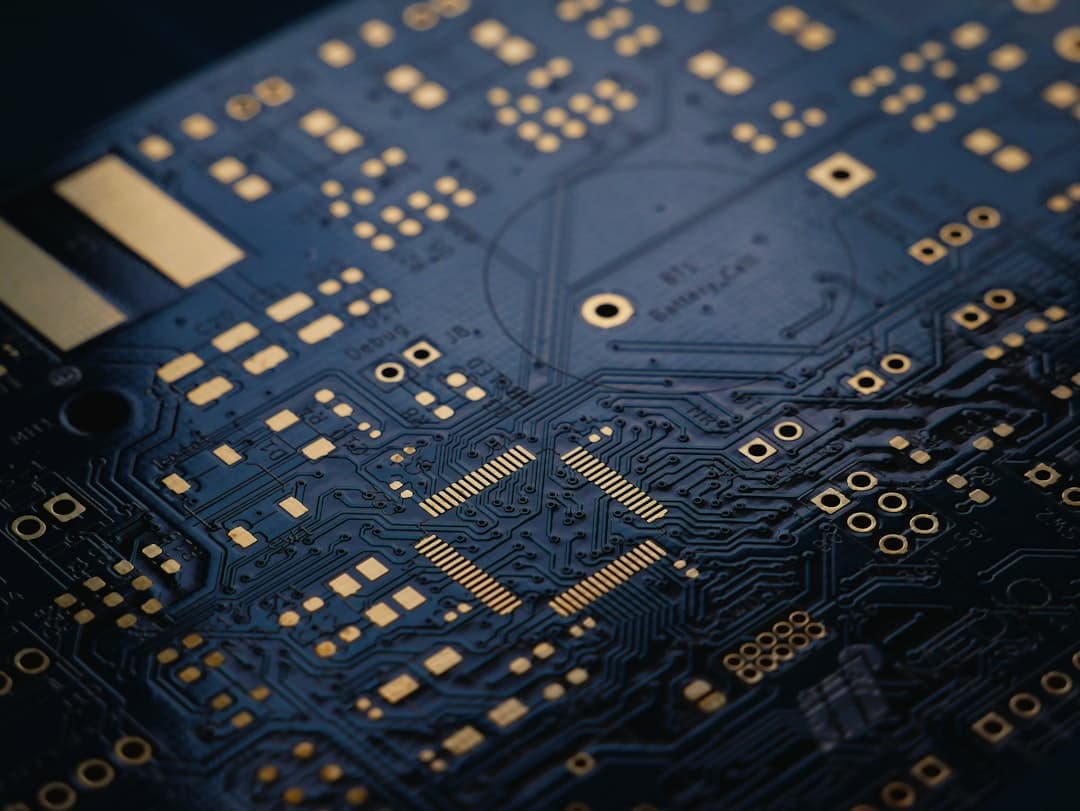

The deeper constraint isn't chip design—it's what sits underneath. Some 60% of the world's PCBs come from China, and nearly all AI circuit boards for Nvidia and others are made in China , creating supply chain vulnerabilities that have drawn the attention of the U.S. Defense Department. Printed circuit boards are the foundation on which every AI chip sits, and they present opportunities for adversaries to sneak through malicious components, creating national security concerns so significant that the U.S. Defense Department is requiring most of its purchases to come from domestic factories .

New legislation would offer a 25% tax credit and $3 billion for U.S. PCB makers like TTM, according to CNBC. But the immediate problem is capacity, not incentives. The PCB production process takes up to six months and requires a lot of power and water . Even with subsidies, domestic production won't scale fast enough to meet 2026 demand.

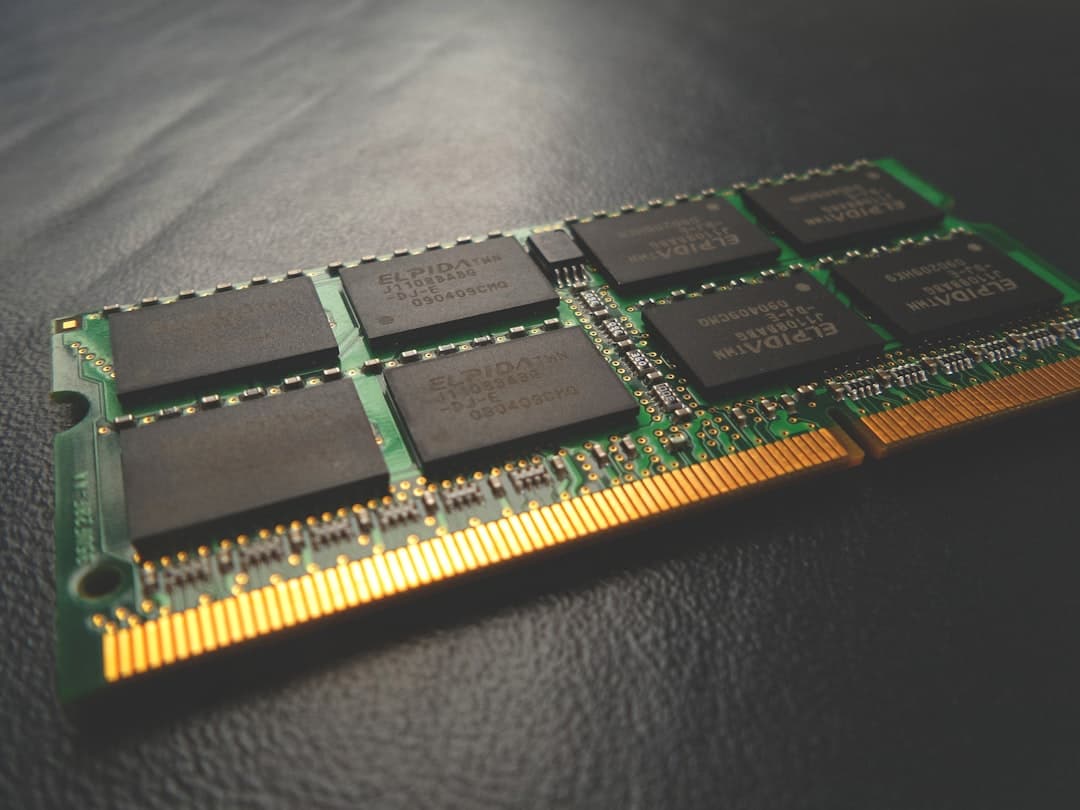

The memory shortage is worse. SK Group Chairman Chey Tae-won stated at Computex 2026 that the global shortage of high-bandwidth memory chips will persist through at least 2030, driven by AI systems that require far more wafer capacity per chip than conventional DRAM . Nvidia CEO Jensen Huang walked to the SK Hynix booth at Computex, picked up a marker, and wrote "Please Make More" on an HBM4E wafer on display, according to TechTimes. The world's most valuable company is publicly begging its suppliers to move faster.

Nvidia's B300 GPU requires eight HBM chips, each containing 12 individual DRAM dies—meaning a single B300 GPU consumes 96 DRAM dies, and a fully configured DGX B300 system with eight GPUs requires 768 DRAM dies just for the HBM modules alone . Samsung, SK Hynix, and Micron have all been aggressively converting production lines to HBM, as the revenue per wafer for HBM is estimated to be three to five times higher than conventional DDR5 . That economic incentive means consumer electronics—laptops, smartphones, tablets—are getting squeezed. TrendForce expects average DRAM memory prices to rise between 50% and 55% this quarter versus the fourth quarter of 2025 , an increase analyst Tom Hsu called "unprecedented."